Jump to section

![]()

![]()

View Sumitomo Corporation's Sustainability : Climate Change

We put an importance on the international determinations stipulated in the Paris Agreement, and we set “Policies on Climate Change Issues” in order to contribute to achieve the carbon neutrality goal of society in aligned with the Agreement.

The Board of Directors adopted a resolution concerning the Group's policies on climate change issues in 2019 and we have been regularly reviewing our policies. In May 2024, in response to recent changes in the external environment, including climate change countermeasures and energy security, we have updated our equity generation capacity-based ratio target among the Group's climate-related targets. In addition, we have added a commitment to reduce indirect CO2 emissions from general coal mines to zero by the end of 2020s, and to work on natural gas only in projects that contribute to the realization of a carbon neutral society.

The Board of Directors is responsible for making decisions on important management matters based on our Group's climate change-related risks and opportunities, and for supervising the execution of business operations. According to the division of roles stipulated in the Board of Directors regulations, the Board of Directors deliberates and determines on the formulation and revision of climate-related policies and targets, risks and opportunities in the overall business portfolio including climate change related, and the handling of important individual cases, which are submitted to the Board of Directors after review by the Management Council and other bodies.

Also, the Board of Directors receives reports on macro-environmental analyses and responses to climate change issues several times a year and supervises the efforts of the business execution side.

In addition, to ensure that the Company's officers, including directors, are more aware of our commitment to the advancement of sustainability management, evaluation based on the non-financial indicators including “climate change” is used to calculate the amount of the remuneration of officers. For more details, please visit our website “Executive Remuneration Plan.”

Management Council and executive management are responsible for decision-making and business execution of important sustainability-related management matters of the Group according to the company regulations. The Management Council makes comprehensive decisions after consulting with the Corporate Sustainability Committee and other committees in order to assess and manage sustainability-related risks and opportunities and make effective decisions.

In addition, with regard to sustainability-related initiatives and responding to risks and opportunities, the Corporate Sustainability Department, which is a specialized organization in charge of planning and disseminating measures to promote sustainability within the Company, and related corporate organizations such as the Corporate Planning & Coordination Department, which plans the Company's overall management plan and important measures, as well as and the person in charge of sustainability promotion in each business group, and overseas regional organizations work together. Based on information provided by the Company's internal research organizations, the Business Groups, overseas regional organizations, etc., we formulate and promote company-wide plans and measures.

In addition, we have established the Sustainability Advisory Board, which is comprised of outside experts on ESG, to obtain advice and recommendations on our overall sustainability management.

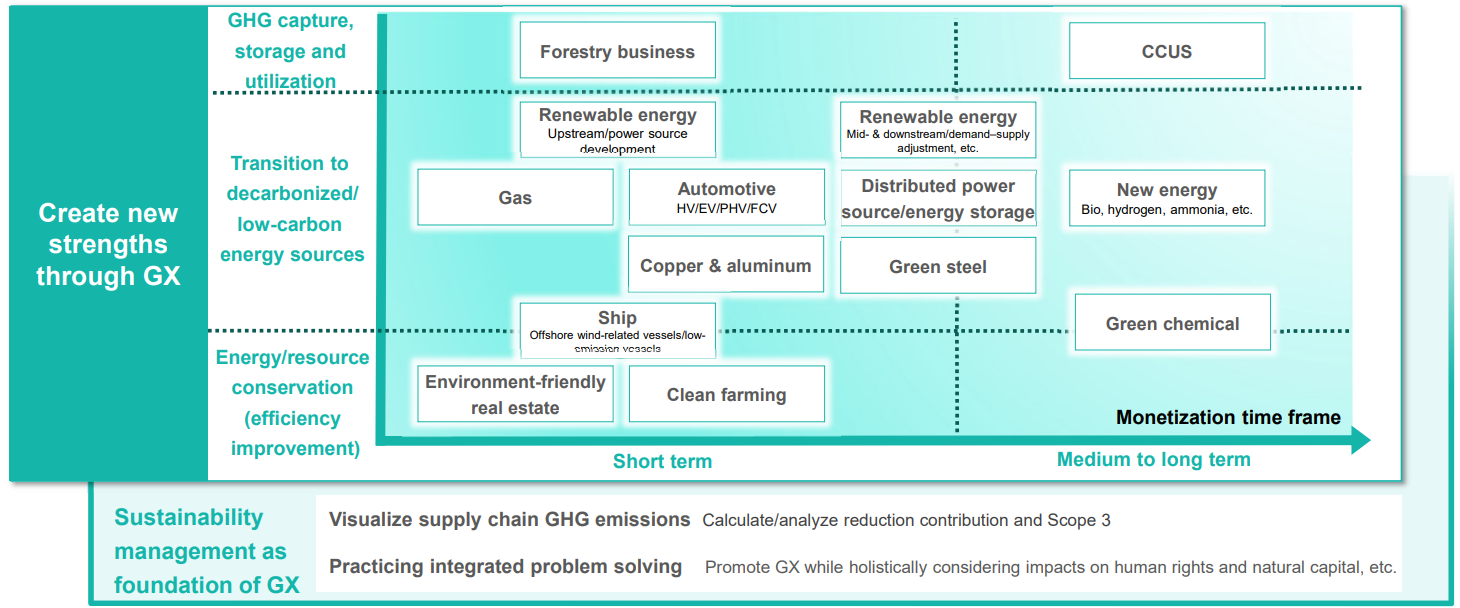

We have promoted the creation of next-generation businesses that contribute to the realization of a carbon-neutral society under prior Medium-Term Management Plan (FY2021-2023), including the promotion of sustainable management and the establishment of EII (Energy Innovation Initiative), a company-wide cross-functional organization. In the new medium-term management plan started from FY2024, we will further strengthen businesses where they have strengths and competitive advantages through green transformation in the short term. At the same time, we pursue green transformation considering time frame to monetization (including market formation) in various industries fields and create new strengths for the future in the mid- to long-term. To this end, we have begun efforts to visualize GHG emissions throughout our supply chain, including the calculation and analysis of Scope 3 emissions. In addition, in addressing climate change issues, we intend to promote GX while taking into account the impact on human rights and natural capital in an integrated manner.

Toward the Group‘s goal of becoming carbon neutral by 2050, we have established specific milestones for CO2 emission reduction as shown in the chart below and are steadily promoting them.

From the perspective of our social responsibility, including the development of local communities and economies and our obligation to supply, we will pursue every option, not eliminating the possibility of accelerated withdrawal from the business, while implementing the following efforts to accelerate the decarbonization of our Company and society as a whole.

| Category | Identified risks and opportunities | Relationship with business models |

|---|---|---|

| Transition risks and opportunities | Risks Our business environment may presumably be affected by introducing regulations for reducing GHG emissions or decarbonization in the future, strengthening international climate actions, updates of each country’s GHG reduction target and changes of technologies and market trends in broad industrial sectors. Opportunities Our business environment may presumably be affected by increase of societal needs for low-carbon and energy-saving products and services and creation of new climate-favored market, corresponding to introducing regulations for reducing GHG emissions or decarbonization and change of preferences of consumers. |

Business models with relatively higher risks described left are electricity generation and energy resource; automobile; aircraft; shipping; steel; chemicals; cement; aluminum smelting; real estate.Throughout the analysis on these business models, we periodically recognize risks to affect our business activities in taken up business models and gravity of the risks and consider implementing necessary measures to minimize negative impacts on our performance. In order to take advantage of opportunities, we have been strengthening our business activities to contribute to realizing a carbon neutral society by formulating strategies including investing in potential businesses such as next generation energy and increasing evaluations of existing climate-related businesses through improving business efficiency. |

| Physical risks | Chronic physical risks Our business environment may presumably be affected by occurrence of average temperature increase, precipitation pattern change and sea level rise in a continuous and chronic manner. Acute physical risks Our business environment may presumably be affected by intensification of extreme whether events such as storms, floods, droughts, and forest fires in an acute manner |

We analyzed physical risks described left focusing on power generation including renewable energy,upstream energy resource, real estate, agriculture and forestry businesses as areas with relatively higher physical risks in terms of possessing larger scale assets or requiring more natural resources for their operation.We manage these physical risks by assessing impacts related to local weather conditions and geological factors before investing, conducting continuous assessment after involved, clarifying scope of contractual responsibility and securing coverage of damage insurance. |

:Significant increase to increase

:Significant increase to increase :Increase to Slightly increase

:Increase to Slightly increase :Neutral

:Neutral :Slightly decrease to decrease

:Slightly decrease to decrease :Decrease to Significant decrease

:Decrease to Significant decrease| Referenced scenarios (Macro Environment) |

||||

|---|---|---|---|---|

| Sector | Business | 2030 | 2050 | |

| Energy | Thermal power generation (coal) | |

|

|

| Thermal power generation (gas) | |

|

||

| Renewable energy power generation | |

|

||

| Next generation energy | Hydrogen, ammonia, synthetic fuels | |

|

|

| Storage battery, energy management | |

|

||

| CCUS | |

|

||

| Resources | Thermal coal | |

|

|

| Coking coal | |

|

||

| Iron ore | |

|

||

| Natural gas and LNG | |

|

||

| Nickel | |

* | ||

| Copper | |

* | ||

| Transportation | Vehicles | |

* | |

| Shipping | |

|

||

| Aviation | |

|

||

| Material industry sector | Steel | Steel sheets | |

|

| Tubular products | |

|

||

| Cement | |

|

||

| Chemicals | |

|

||

| Aluminum | |

|

||

| Real estate sector | Office buildings / residential building sales business | |

|

|

| Other | Forestry | |

|

|

Thermal power generation (coal and gas) businesses

Regarding coal-fired power generation, there is a gradual decline starting in developed countries and in all scenarios, there is a significant decline by 2040 or 2050. While gas-fired power generation as a percentage of total power generation will decline over the medium to long term, we expect that investigations will continue into reducing CO2 emissions through the use of hydrogen, CCUS, and other new technologies. However, to advance the energy transition, we expect gas to remain an important power generation source because, from the perspective of stability of power supply, a certain level of gas-fired power generation will be required.

We have set policies on power generation businesses*1 and we have been shifting our allocation of management resources from thermal power to power generation businesses with low environmental impact, such as renewable energy.

We believe that gas-fired power generation is an important power generation method that will play a bridging role in the energy transition, and a dispatchable power supply role to support power supplies as renewable energy power generation spreads. We also have high expectations, and are implementing initiatives, for innovative low-carbon technologies, including the use of green hydrogen, to help achieve carbon neutrality. While contemplating the development of local communities and economies and our obligation to supply electric power as stabilized power supply, we will pursue various options, without eliminating the possibility of accelerated withdrawal from the business to realize decarbonization of our company and society as a whole. We will pursue the decarbonization and low-carbonization of existing facilities and providing maximum support for host countries to shift power sources to renewable energy and other sources. We are utilizing our extensive know-how in power generation businesses to deliver high-efficiency, high-quality power supplies with outstanding environmental performance in countries around the world.

<Reference>

| Coal-fired power generation business*1 | As of Mar. 31, 2025 | Estimate for 2035 | Latter half of the 2040s |

|---|---|---|---|

| Outstanding investments, loans and guarantees*2 | 320 billion yen | Approx. 150 billion yen | Zero |

| Net ownership generation capacity | 5.2GW | Approx. 2GW | Zero |

Renewable energy power generation

With an increasing trend toward carbon neutrality, the use of renewable energy as a main source of power is accelerating around the world. In addition to renewable energy such as solar, wind, and geothermal power generation, the demand for renewable energy to produce green hydrogen is also increasing. In each of the scenarios to the left, renewable energy power generation output increases dramatically by 2050, while it is forecast to increase roughly eightfold from the current output in the NZE scenario.

To overcome the issue of climate change and bring about a carbon neutral society, the Sumitomo Corporation Group is engaged in various renewable energy businesses such as wind, solar, geothermal, hydroelectric, and biomass. While providing the stable supply of energy essential for the development of economies and industries in local societies, we are putting forward a policy of continuing to shift management resources to a power generation portfolio with low environmental impact, such as renewable energy. We also aim to achieve net generation capacity of 5 GW or more for renewable energy by 2030. As of the end of March 2025, our net generation capacity is approximately 2GW which is a steady progress, mainly from offshore wind power in Europe. In addition to growing our solar and wind power generation businesses, we are also promoting hydroelectric power generation businesses in regions where there is an abundance of water resources, and we are promoting operation and development of geothermal power generation businesses in Indonesia, a country with the world’s second-largest reserves of geothermal resources.

Carbon-free energy (hydrogen, ammonia, synthetic fuels, etc.) development businesses

Demand for next-generation energies as fossil fuel alternatives that contribute to reduced lifecycle CO2 is increasing. In all IEA scenarios, clean energy investment is projected to account for the majority of energy investment in 2030. On the supply side, in areas where natural gas and renewable energy are rich and available, global investment plans are already in place for development of hydrogen and ammonia plants. On the demand side, governments in Europe, Japan and Asia are formulating plans to use hydrogen and ammonia to realize decarbonization in industry. Government support frameworks, technology development, and social acceptance are essential to establish successful business.

In FY2021, we launched the Energy Innovation Initiative to promote the development of businesses related to hydrogen, ammonia, synthetic fuels, and other next-generation energies as an important focus area. As for hydrogen, for instance, we have been engaged in developing hydrogen-related businesses from various perspectives, such as projects for locally produced and consumed hydrogen that take advantage of the characteristics of locales and of hydrogen itself, large-scale hydrogen value-chain projects that promote the mass production, transportation, storage, and utilization of hydrogen, and investments in new technologies.

We will build supply chains based on optimal technologies, cost, and timeframes for each next-generation energy and contribute to realize a decarbonized society by ensuring the stable supply of next-generation energies.

Storage battery and energy management businesses, etc.

If current government targets and policies around the world are promoted, electric vehicles will apparently reach market share of 45% globally. There will be a much greater need for storage batteries that have high energy and storage efficiency, so from the perspective of energy management as well, the market is forecast to expand to around 10 times of the current market size. In line with this, European battery regulations are moving to require storage battery recycling, carbon footprint disclosure, and traceability. In addition, with an uneven geographical distribution of mining for the critical mineral resources used in batteries, there is a risk that increased prices for cobalt, lithium, and nickel will cause the price of storage batteries to increase.

To secure stability of power networks, which is a major challenge for greater spread of renewable energy, we are commercializing new energy management technologies that use storage batteries. As another key to mitigating climate change, we are also promoting businesses that reduce energy consumption and utilize renewable energy on the energy demand side, such as the car sharing business. Specifically, by developing businesses ourselves utilizing our accumulated know-how and internal resources within Sumitomo group including electricity wholesale and renewable generation development, we manage project development and operation from economics point of view and improve project revenues from our electricity service businesses. In this way, we are strategically ensuring commercial viability of those businesses and promoting trials of new ideas in society. Going forward, we will also consider contributing to further utilization of vehicle storage batteries around the world.

CCUS*1 adoption business

CCUS is a new technology, so the spread of such technology is limited at present. However, with a range of support including subsidies and tax deductions in Europe, the United States, and other developed countries, investment is growing. In the NZE scenario, a high need for CO2 capture is forecast for 2030 due to new construction and refurbishment of blue hydrogen manufacturing equipment, coal-, gas-, and biomass-fired power plants, and cement, steel, chemicals and other industrial facilities. Thus, CCUS adoption globally is forecasted to increase. At the same time, the idea of cross-border CO2 transport from high-emitting countries to countries with large carbon storage capacity is also being considered in Asia and some European countries. On the other hand, unlike the referenced scenarios, if there is a global softening of CO2 reduction initiatives, potential risks include shrinking markets, cessation of subsidy schemes, and increasing costs associated with capital investment.

The existence or otherwise of subsidy schemes in the future will greatly impact the economic efficiency of the business and the feasibility of establishing it. Therefore, in countries and regions that are already starting to develop frameworks for subsidies, we aim to actively utilize those frameworks, participate in projects at an early stage, and build up a track record. Specifically, these include acquiring CO2 storage sites in the UK, promoting joint CCS project development with local partners in Canada, and considering cross-border CO2 exports between Japan and Australia. On the other hand, in countries and regions that are establishing carbon emission targets and considering related policies, we aim to develop a market and create projects from our accumulated expertise, by collaborating with governments and being involved in the establishment of legislative systems as much as possible. We are also working to build a CCUS value chain through the creation of carbon removal credits. Specifically, we have invested in Inherit Carbon Solutions AS, a Norwegian company that develops CDR from biogenic CO2, and we are also investigating a DAC*2 business in the Americas with Tokyo Gas Co., Ltd.

Upstream

The energy policies of many countries, especially developed countries, include plans to shift from coal-fired power generation to gas-fired power generation and then renewable energy, so demand for the thermal coal used in coal-fired power generation is forecast to decline.

We will not acquire new interests in the thermal coal mine development, and we plan to reduce equity production volume from thermal coal mines to zero by the end of 2020s. The weight of thermal coal interests in our resource portfolio is relatively small. Going forward, mines of currently owned interests are scheduled to reach the end of their mine life in the near future. Also, the concession produces high-grade coal, which is in relatively high demand, and is cost-competitive, making it resistant to price declines even when there is a drop in demand.

<Reference>

As of March 31, 2025 Thermal / coking coal Exposure: 80 billion yen

Upstream

In the long term, many countries and regions will develop policies for adopting or strengthening carbon taxes, so demand for coking coal is forecast to decline as low-carbon iron-making processes with fewer CO2 emissions are put to practical use and the ratio of electric furnace use increases.

In combination with CCUS and other CO2 capture and storage technologies, it is predicted that steel businesses that use blast furnaces will be preserved for the time being. In addition, we believe that a certain level of demand will be maintained for the interests we hold as they produce hard coking coal, which is considered rare among coking coals.

<Reference>

As of March 31, 2025 Thermal / coking coal Exposure: 80 billion yen

Upstream

Despite a forecast gradual increase in global demand for steel, an increase in the ratio of electric furnace steel as a result of moves toward decarbonization may lead to a portion of raw materials being replaced with steel scrap and a decline in overall demand for iron ore. On the other hand, demand and production of direct reduced iron is forecast to increase as a way to reduce CO2 emissions in both the blast furnace method and the electric furnace method, so demand for the high-grade iron ore used as raw materials for direct reduced iron may increase.

Regarding our iron ore-related businesses, through our projects in South African and Brazilian mines, we contribute to stable supply of resources to Asia, with a focus on China and Japan. We will continue to take actions for stable supply while paying close attention to the impact on demand due to changes in the iron-making and steelmaking methods in response to decarbonization in the steel industry, and also to the impact of an increase in the ratio of electric furnace steel.

Upstream, midstream and downstream, trading of natural gas/ LNG

Despite a significant gap in demand increase/decrease between each of the scenarios, natural gas will be used as an alternative power fuel for coal in the transition phase to a low-carbon society. In addition, it will continue to play an important role as a raw material for petrochemical products, ammonia, and fuel for transportation.

In the short to medium term in particular, demand is forecast to increase in the ASEAN nations, and it is expected that business opportunities will increase in the Asian Pacific (including India) and China. The main supply-side countries and regions for LNG in the future may be the Middle East and United States and, with the impact of the conflict between Russia and Ukraine, LNG trade opportunities with demand-side countries and regions may increase.

In the long term, the spread of renewable energy will offset increased demand in emerging countries, so demand is forecast to trend downward. However, a certain level of demand for natural gas is forecast to remain in some countries and regions where the use of renewable energy is not suitable, so natural gas will continue to play an important role in the best mix of renewable energy, such as a balancing function when renewable energy is not available.

We will focus on strategic regions from the medium to long-term perspective, and we will work to maximize opportunities by creating a natural gas and LNG value chain in combination with upstream LNG projects, LNG trading, and midstream and downstream businesses. Furthermore, we will contribute to the stable supply of energy to the appropriate countries and regions while securing demand for transition fuels which support the shift to a carbon neutral society while introducing environmental technologies such as CCS/CCUS and promoting the best mix of renewable energy sources.

<Reference>

As of March 31, 2025 Gas, LNG Exposure: 80 billion yen

Upstream

With the spread of renewable energy, EVs, and storage batteries, which are essential in the expansion of low-carbonization and decarbonization, demand for the nickel used in rechargeable batteries is forecast to increase dramatically in the medium to long term.

We are proceeding with projects as a producer in the Republic of Madagascar. We sell the products to Japan, Europe, North America, and Asia, and we are aiming to create further business opportunities. While continuing to conserve biodiversity, including reforestation of quarries, and conserve the environment surrounding mines and plant sites, we will also continue to find and implement CO2 emission reduction measures, and work to stabilize production and increase production volumes.

Upstream

With the spread of renewable energy and EVs, demand for copper is forecast to increase in the medium to long term. On the other hand, increasing supplies is forecast to be difficult due to increasing risks and difficulty of operating newly developed mines, and impacts of things like a tightening of environmental protection regulations.

We will continue to contribute to stable procurement of copper products by acquiring new concessions and expanding production at existing concessions through investment in copper mines overseas, and by strengthening our operations on the copper production value chain. These include our upstream copper concentrate production business and midstream copper bullion production and sales business. We will also continue working to conserve the environment around our mines by monitoring rare species living in the vicinity of the mine, for instance.

Sales of automobiles, manufacture and sales of automobile components, automobile finance, automobile leasing, car sharing, parking lot operation, etc.

Sales of passenger cars are forecast to increase, especially in emerging countries, and the ratio of EV sales in new car sales are forecast to increase as fuel efficiency regulations tighten. In terms of automobile components, demand for internal combustion engine parts is expected to decline in the future with the spread of EVs, but demand for tires is expected to increase with the associated increase in automobile body weight. If car prices increase as a result of the introduction of carbon tax and so on, there is a risk that new car sales will decline. At the same time, however, demand for automobile finance and leasing businesses is forecast to increase.

In addition to manufacturing and selling automobiles and automobile components, we are engaged in a wide range of businesses in the MaaS field. We see the spread of EVs and developments in MaaS as business opportunities. For example, as part of our parking business in Northern Europe, we are expanding the charging networks essential for the spread of EVs and the EV subscription services using our parking facilities. In Japan, we are working on new business opportunities such as providing fleets of EVs for commuter use, workplace charging facilities, and solar power generation services. Demand for internal combustion engine parts is expected to decline with the spread of EVs, but we consider ourselves to have a limited financial exposure as these parts account for less than a few percent of our parts manufacturing business. We are investigating and implementing a range of initiatives, such as use of carbon-free energy and low-carbon and carbon-free technology to contribute OEM’s supply chain carbon neutrality.

Shipbuilding, trading, ship owning and operation

Shipping demand is expected to increase steadily over the medium to long term due to the development of modal shift and other factors. While the cost of investment in low-carbon technologies and the cost of operation could both increase as a result of GHG emission regulations and taxes by IMO*1 and authorities in each country, the need for zero-emission and low-emission ships*2 are also forecasted to increase.

While monitoring the legal regulations and markets in each country, as well as trends in zero-emission and low-emission ships technologies and costs, we are working to increase the ratio of low-emission ships in our shipbuilding business product lineup and ship owning portfolio in expectation of future adoption of regulations.

Furthermore, we have been working on the joint development of an ammonia-fueled ship through the partnership with Oshima Shipbuilding. Also, we are investing in offshore windfarm support vessels, a new field expected to see growing demand in the future. In this way, we will create new business opportunities for achieving decarbonization and low-carbonization in society.

Commercial aviation and engine leasing, manufacturing aircraft components, aircraft part-out, carbon credit trading, etc.

Aviation demand is forecasted to increase over the medium to long term. There is a shift toward fuel-efficient aircraft due to ICAO*1 and IATA*2 regulations, and the start of the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). At the same time, in the medium to long term, the introduction of SAF*3 and the demand for carbon credits are expected to increase.

In our mainstream commercial aviation and engine leasing businesses, we are working to achieve sustainable revenue growth by replacing aircraft and engine portfolio with better fuel-efficient ones and capturing leasing demand for addition and replacement of airline customers. We are also contributing to customer (airline) initiatives toward decarbonization. By shifting our portfolio while monitoring market and technology trends and legal legislations regarding aircraft fuel efficiency, we will respond flexibly to changes in the business environment and manage the risk of decrease in leasing fees and prices of our owned aircraft.

We are promoting efforts that contribute to the creation of a circular economy through the aircraft part-out business, selling dismantled parts from retired aircraft. In addition, as for carbon credits, SAF and other biofuels, we are working on commercial production to begin. In this way, we are striving to reduce CO2 emissions in society while aiming to acquire business opportunities at the same time.

Trading and investment of steel flat rolled products and tubular products, and other steel products

Although the direct impacts of climate change and global warming are limited, indirect impacts such as the partial conversion of steelmaking processes, in which there is an increasing need to reduce CO2 emissions, and the development of renewable energy infrastructure and related investments to combat climate change are expected to impact existing trades and businesses, as well as to create new demand and business opportunities. As for steel pipes, although the development of crude oil and natural gas, which are their main applications, is expected to decline in the medium to long term, solid demand is expected to continue for the time being, especially for natural gas, which has a lower environmental impact than crude oil.

Our company will collaborate with strategic partners to promote the sale of green steel products, including the mass balance approach, and explore new business opportunities for greening the steelmaking process and to meet the demand for steel and steel pipes for infrastructure development that contributes to a green circular society." In response to the energy transition pursued by integrated energy companies, which involves the greening and diversification of energy sources, we will promote related businesses and continue to focus on the sale of highly corrosion-resistant steel pipes needed for natural gas development.

Cement distribution business

Global demand for cement is expected to increase due to urbanization and industrialization in emerging countries such as India and African countries, and the expansion of new infrastructure facilities such as green energy mainly in mature countries. If climate change mitigation progresses, the increase in cement demand is expected to be smaller due to focused measures on more efficient material, but overall it is expected to remain flat.

While there is a risk of increased costs and reduced demand due to the introduction of regulations promoting decarbonization of conventional cement, which has high CO2 emission, there is also an opportunity of increased demand for cement produced using low-carbon methods.

Our company is involved in the cement distribution business, which does not include the cement manufacturing process. Therefore, our own CO2 emissions are limited.

We will develop a sales strategy in response to market changes in order to capture the growth in the conversion of fuels in cement production to clean energy and the increase in distribution of low-carbon cement that replaces the main raw material limestone with other materials.

We are also collaborating with promising cleantech companies to verify clean cement production technologies and develop related products using those technologies.

Manufacturing, trading

Chemical demand is expected to increase with the expansion of renewable energy and energy-related infrastructure. On the other hand, naphtha produced by refining petroleum is used as the principal raw material, but in the long-term process of energy decarbonization, the supply of naphtha used as raw material is expected to decline. In addition, CO2 is emitted in huge volumes from fossil fuel energy used in the synthesis and decomposition processes of petrochemical product manufacturing, so demand for low-carbon manufacturing processes, including shifting energy used in the processes to renewable energy, is expected to grow.

We have been monitoring customer demand for decarbonization, and trends in relevant technologies, and exploring business opportunities in chemical product manufacturing using biomass materials and CCU (CO2 capture and utilization). For example, in 2024, we have started trading petrochemical products using bio-naphtha as the main raw material, in response to structural changes in the petrochemical industry. In addition, we will continue our global trading by adjusting to changes in supply and demand in petrochemical product raw materials and finished product markets.

Smelting

Because of its lightness and excellent recyclability, aluminum is an essential metal for decarbonization of society, including improving fuel efficiency of automobiles by reducing vehicle weight, so demand is forecast to increase. On the other hand, large amounts of electricity are consumed in the primary smelting process, so in a future society promoting low-carbonization and decarbonization, demand for green aluminum*, manufactured using electricity from renewable energy and other methods to reduce CO2 emissions, is forecast to increase.

Our aluminum smelting business in Southeast Asia chiefly utilizes renewable energy derived from hydroelectricity, so future risks pertaining to carbon pricing is expected to be limited, and the business is likely to remain competitive in the medium to long term. For this reason, future demand for decarbonization in the supply chain from end-users is expected to present business opportunities where Sumitomo Corporation is able to utilize its strengths. We will work toward strengthening our competitiveness by further expanding our interests in green aluminum and increasing volumes we handle.

Office buildings, commercial facilities, residential housing, distribution facilities and real estate funds

Demand in the real estate sector is forecast to increase in light of population increases and urbanization in emerging and developing countries and increasing refurbishment of existing buildings. On the other hand, a major challenge for buildings is to reduce CO2 emissions by reducing energy consumption.

In Japan, in order to achieve carbon neutrality by 2050, energy-saving performance equivalent to the ZEH/ZEB standards will be required for new properties after 2030 as part of demand for CO2 emission reductions through improved energy efficiency. If unable to meet these requirements, the risks are that real estate prices will fall, and demand will decline due to increased operating costs. However, meeting the requirements offers opportunities for increased earnings as demand for ZEH/ZEB-compliant building increases and property values increase.

We are involved in development and operation of a range of real estate properties. To reduce both embodied carbon, which is emitted through construction, and operational carbon, which is emitted during the use of buildings, we are utilizing existing structures, adopting the latest equipment including smart meters and EMS, updating facilities, and introducing renewable energy both onsite and offsite, based on trends in customer demand and technologies. In addition, we are cooperating with tenants to implement environmentally friendly initiatives and working on acquiring environmental certification and developing properties to the ZEH/ZEB standards.

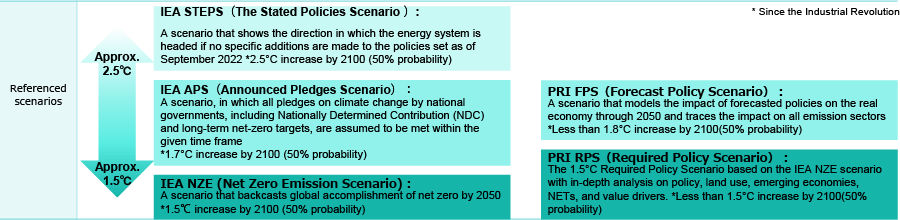

* The NGFS (Network for Greening the Financial System) scenarios of Current Policies, Delayed Transition, and Net Zero 2050 closely approximate the temperature ranges of the STEPS, APS, and NZE scenarios, respectively.

Forestry business

With the trend toward carbon neutrality, the United Nations, COP26, and national governments are establishing many targets for such objectives as stopping forest destruction and land degradation, and increasing forest protection and the size of forest areas. In all scenarios, forest area is expected to slightly increase by 2050.

Under these circumstances, while monitoring of illegal logging and activities that can lead to deforestation will be strengthened, we believe that sustainable forest management and timber supply will increase in value.

Also in the future, demand is forecast to increase for carbon removal credits that recognize absorption of CO2 in forest cultivation processes, and for alternatives to petrochemical products by using low environmental impact forest products from sustainable logging. We therefore expect competition around investment and development will intensify among countries and companies in this field.

We established the Forest Management Policy and the Sourcing Policy for Forest Products in 2022 as part of efforts toward sustainable forest management and sourcing of forest products. We also set Operational Guidelines for putting the policies into actions and conduct annual monitoring in accordance with these guidelines.

In line with these policies, we will expand our forestry business on the assumption of sustainable forest management. While supplying conventional forest products, we will also work to develop new products and businesses that contribute to the capture, storage, and utilization of CO2.

The projections and forecasts contained here are based on information available as of the date of this announcement, and on certain assumptions and projections. Therefore, actual results and performance may differ significantly due to various uncertainties, including future economic trends and market prices. Neither the company nor the information providers assume any responsibility for any errors in the information posted or for any damages incurred based on the information presented.

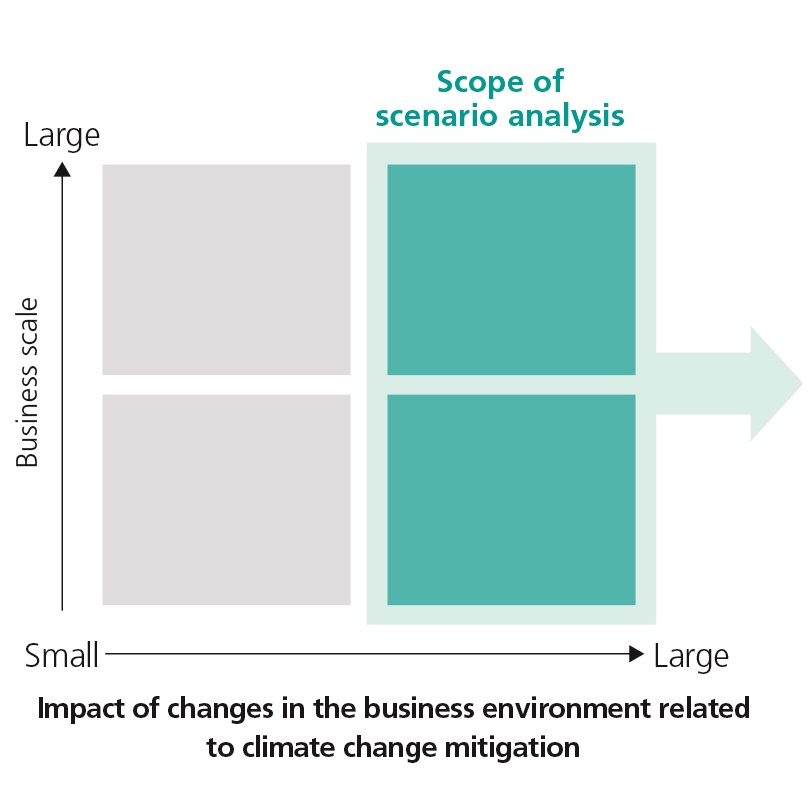

Each year, we identify the Group's sectors and businesses affected by physical risks and inspect the status of their response to these risks. In particular, for businesses with large outdoor sites or those that require large amounts of natural resources for operations, we use assessment tools to analyze the degree of impact of physical risks and individually check the status of their response.

Since the Group operates in a wide range of sectors around the world, we refer to UNEP FI reports describing the impact of physical risks on major sectors, as well as other reports. We identify the major risk characteristics for each of our sectors that are likely to have a significant impact, as well as the major businesses we are involved in, as shown in the table below. This year, we have added forestry to this list.

Physical risks are largely divided into chronic risks that have continuous and chronic impacts on business activities, (e.g., rise in average temperatures, change in rainfall patterns, rise in sea level, etc.) and acute risks caused by unforeseen damage (e.g., escalation of extreme weather conditions such as huge rainstorms, flooding, drought, and forest fires, etc.). The impact is wide-ranging, including direct impact on production site facilities and working conditions, and indirect impact on a broad range of supply chains of raw materials and products. For our business in a broad range of fields and regions, we manage such risks by assessing the impact of local weather and geographical factors on our business at the time of investment, conducting continued assessments after participation in the business, clarifying the scope of contractual responsibility, and concluding nonlife insurance policies.

| Sector | Awareness of the impact of physical risks in each sector | Principal business related to the risk described at left | |

|---|---|---|---|

| Chronic | Acute | ||

| Energy | Water shortage resulting in decline in production efficiency and in operation efficiency, risk of submergence due to sea level rise, etc. | Damage on facilities, disruption of operation, etc., caused by flooding and huge rainstorms | Thermal power generation in Southeast Asia, Middle East and Africa, Wind power generation in Japan and overseas, biomass power generation in Japan, solar power generation, and other renewable energy generation businesses, etc. |

| Resource & Interest | Rise in temperature & water shortage resulting in decline in production efficiency, disruption in operation, risk of flooding with rise in sea level, etc. | Damage on facilities, disruption of operation, etc., caused by flooding and huge rainstorms | Mining operations in North America, South America, Australia, Africa, etc.; energy interests in Southeast Asia, Middle East & Europe; and sales of such resources and energy |

| Raw materials | Rise in temperature & water shortage resulting in decline in production efficiency, disruption in operation, etc. | Damage on facilities, disruption of operation, delay in raw materials/product shipment, etc., caused by flooding and huge rainstorms | Manufacturing, processing, sales, etc., of metal products, transportation equipment and parts, chemical products, materials, etc. |

| Transportation systems | Water shortage resulting in decline in production efficiency, disruption of operation, etc. | Damage on facilities, disruption of operation, delay in raw materials/product shipment, etc., caused by flooding and huge rainstorms | Manufacturing and sales, etc., of transportation equipment and parts |

| Real estate | Delay in project schedule, rise in utility cost, decline in property value with a rise in sea level, etc., resulting from rising temperature | Delay in project schedule, decline in property value caused by structural damage & flooding, etc., caused by flooding and huge rainstorms | Office building business, retail facilities business, residential business, logistics facility business, etc. |

| Agriculture | Rise in temperature & climate change resulting in decline in production efficiency, etc. | Disruption in operation, etc., caused by huge rainstorms, flooding or drought | Agriculture & import and wholesale of food products, retail sales business, etc. |

| Forestry | Temperature change resulting in changes in the growth environment, etc. | Decline in asset value of forest resources, etc., caused by natural disasters | Forestry business in Russia, New Zealand, etc. |

While physical risk includes a variety of risks, we have conducted a more detailed risk analysis of the sectors and businesses identified on the previous page as being susceptible to physical risk based on the factors such as having large outdoor locations or requiring a large amount of natural resources for operations.

In addition to power generation, upstream resources and energy, real estate, and agriculture businesses, we also conducted a risk analysis of forestry businesses this year using assessment tools such as the RCP8.5 scenario*1 based on the IPCC*2 scenario of a 4°C rise by 2100, mainly in terms of water stress, flooding and sea level rise, temperature rise, and forest fires, based on information such as the geographical information of major business sites, while considering the actual conditions of the businesses. For these businesses, we also confirmed that risk management was being conducted appropriately by assessing the impact of local weather and geographical factors on our business at the time of investment, conducting continued assessments after participation in the business, clarifying the scope of contractual responsibility, and concluding nonlife insurance policies.

| Sector | Analysis Results and Status |

|---|---|

| Energy | Analysis of water stress on power generation business showed there areregions with possible water shortage. However, water used in our thermal power generation business, which uses large amounts of water for cooling, is supplied by seawater, water production facilities within the power plant, etc., leading to the conclusion that the risk of operation disruption caused by water shortage, etc., is not significant. |

| Resource & Interest | In the study of the resource & interest business in terms of water stress and continual temperature increase risk, there are regions found to have relatively high risk of long-term increase in the number of days when temperature reaches 35°C or higher and possibility of water shortage. Sumitomo Corporationplans to execute risk control through assessment of disaster risks vis-à-vis geographical conditions, etc., definition of working conditions with sufficient attention to temperature and other conditions, subscription to nonlife insurance, etc. |

| Real estate | In the real estate business, sufficient research and analysis are being conducted on flooding risks for various locations during the development studies stage. Property projects are being selected through conservative assessment of risks based on information from hazard maps and specific conditions of each property site, etc. In promoting project development, measures are being taken on physical risks in order to minimize them. For this reason, risks in the business portfolio as a whole are not considered significant. |

| Agriculture | In the analysis of temperature rise and water stress for major agricultural sites in each country, there are regions with a possible increase in the number of days when temperature rises to 35°C or higher andpossible water shortage. Although adverse impact is anticipated on such agricultural operations if such risks affect agricultural product quality, output, etc., Sumitomo Corporation has diversified crops and regions in the business and has therefore built risk resistance to a certain degree in terms of total performance. |

| Forestry | In the analysis of forest fire risk in the forestry business, it was confirmed that the risk is low for the forest assets currently owned by the Company. For our forests, we are taking measures in accordance with fire prevention plans, etc. |

The Group set “Policies on Climate Change Issues” and long- and medium-term goals for Material Issues, and aim for realizing carbon neutrality by 2050 as well as contributing to carbon neutrality of society. The main points made in the policy and in the long-term and medium-term goals are as follows. Please check “Policies on Climate Change Issues” and “Material Issues” for details.

From April 2023, we have been operating an internal carbon pricing (ICP) system to calculate carbon emission costs. We utilize analysis from the system to consider companywide measures to create new climate-related business opportunities and check potential impacts on future businesses for decisions on investment.

In the ICP system, we use the outlook on carbon price of the Net Zero Emission Scenario (NZE) in the World Energy Outlook 2024 published by the IEA for conducting scenario analysis according to the location of new and existing projects.

<Carbon price in our ICP>

($/t-CO2)

| 2030 | 2035 | 2040 | 2050 | |

|---|---|---|---|---|

| Advanced economies with net zero emissions pledges | 140 | 180 | 205 | 250 |

| Emerging market and developing economies with net zero emissions pledges | 90 | 125 | 160 | 200 |

| Selected emerging market and developing economies (without net zero emissions pledges) | 25 | 50 | 85 | 180 |

| Other emerging market and developing economies | 15 | 25 | 35 | 55 |

(Thousand t-CO2e)

| Index | Result of FY2019 (The base year) | FY2024 | Percentage of change | Reduction targets of 2035 | |

|---|---|---|---|---|---|

| Entirety | 59,939 | 50,845 | ▲15.2% | 50% or more | |

| Sumitomo Corporation and its subsidiaries (other than power generation)*2 | 1,005 | 672 | ▲33.2% | - | |

| Power generation business*3 | 43,126 | 38,610 | ▲10.5% | 40% or more | |

| Of which, coal-fired power generation*3 | 34,452 | 32,429 | ▲5.9% | 60% or more | |

| Fossil energy concession*4 | 15,808 | 11,564 | ▲26.8% | - | |

| Of which, thermal coal mine interest | 12,538 | 10,248 | ▲18.3% | Zero emissions by the end of the 2020s | |

(MW)

| Index | Result of March 31, 2020 (The base year) |

Result of March 31, 2025 | Targets of 2030 |

|---|---|---|---|

| Renewable energy* | 1,397 | 2,152 | 5,000 or more |

(MW)

| As of March 31, 2025 | |

|---|---|

| Coal-fired power generation | 5,172 |

| Gas-fired power generation | 2,674 |

| Renewable energy*1 | 2,152 |

| Total | 10,001 |

Among power stations sourced by renewables such as solar, wind, biomass and geothermal energies, solar (photovoltaic) power plants generate the greatest amount of electricity in Japan. So called "mega-solar (far-over-MW photovoltaic)" power plants started to be constructed across the country in 2012, after the introduction of the Feed-in Tariff system.

In the 1990s, Sumitomo Corporation began importing polysilicon and other materials for Japanese photovoltaic panel manufacturers, while exporting their products to overseas markets. We subsequently started the development of mega-solar power plants in Europe and the United States, and from 2012, in Japan. Today, we own and operate mega-solar projects at six locations nationwide.

Construction of wind power plants came into full swing in Japan in the early 2000s, before mega-solar projects gathered momentum. Sumitomo Corporation started the commercial operation of its first wind power plant in 2004, when wind power generation had just begun to take off. We then launched several projects, including those in Kashima, Ibaraki Prefecture and Oga, Akita Prefecture, which are well into the operational stage today. In April 2025, a new onshore wind farm—among the largest in Japan—officially commenced commercial operations in the Abukuma region of Fukushima Prefecture.

In April 2025, under the Fukushima Renewable Energy Promotion Vision and the Fukushima New Energy Society Concept, the Abukuma Wind Power Plants No.1, No.2, No.3, and No.4 (hereinafter collectively referred to as "the Abukuma wind farm"), which had been under construction since April 2022, officially commenced commercial operations under the Feed-In Premium (FIP / *1) system.

The Abukuma wind farm is one of Japan's largest onshore wind farm, with 46 wind turbines, each with a capacity of 3,200 kW, installed on ridgelines in the Abukuma region, spanning the municipalities of Tamura, Okuma, Namie and Katsurao in Fukushima Prefecture. The total generating capacity of the wind farm is approximately 147,000 kW, with an expected annual generation equivalent to the electricity consumption of approximately 120,000 households.

The renewable energy generated at the Abukuma wind farm will be supplied to multiple companies and municipalities with business operations in Fukushima Prefecture through Corporate Power Purchase Agreements (PPA / *2). A portion of the revenue from energy sales will be utilized for funding reconstruction projects in local municipalities where the wind farm is located through the Fukushima Prefecture Renewable Energy Reconstruction Promotion Council.

The Abukuma Wind Power Project will continue to contribute to Fukushima Prefecture’s reconstruction efforts through the stable operation of the wind farm and its returns to the local community. Fukushima Prefecture aims to establish its position as a leading region for renewable energy by generating an amount of renewable energy equivalent to more than 100% of its total energy demand, and this project plays a role in supporting that vision.

Our latest initiative in solar power generation is the development of a mega-solar power plant with a generation capacity of 92,000 KW in Minamisoma, Fukushima Prefecture, which suffered devastating damage from the Great East Japan Earthquake. In 2012, one year after the earthquake disaster, we began drawing up a plan to build a solar power plant with cooperation from the local municipality with the aim of making use of coastal land that subsided due to the tsunami. After overcoming numerous challenges, commercial operation commenced in March 2018 for the first phase of construction, and in December 2018 for the second phase of construction.

Fukushima Prefecture aims to expand its renewable energy power generation capacity to meet 100% of the prefecture's demand by around 2040. Installed on a vast plot of 150 ha land, which is 32 times the size of the Tokyo Dome stadium, the two solar power plants will not only contribute to achieving this target, but also stand as a symbol of restoration from the disaster for the regional people.

Sumitomo Corporation has the vision of operating its plants over the long term, even after the Feed-in Tariff period has ended, to continue supplying environmentally friendly and cost-competitive electricity to society. The prerequisite for fulfilling this vision is to build a relationship of trust with the local communities. The only way our facilities can sustain operations over decades to come is to be accepted and loved by the local people.

Solar and wind power generation is susceptible to weather conditions. As a means of compensating for this weakness and ensuring stable electricity supply, Sumitomo Corporation is looking to use the storage batteries in its renewable energy business in pursuit of optimal electricity management. Furthermore, we are seeking to supply the electricity continuously and stably to consumers, in cooperation with Summit Energy Corporation, a subsidiary engaged in electricity retail business, who own and operate large-scale biomass power plants within the Group.

The Japanese government has set the 2040 target for the proportion of renewable energy in the domestic energy consumption mix to up to 40~50%. The Sumitomo Corporaton Group meanwhile, has a medium-term goal of increasing its renewable energy power supply capacity to at least 3 GW in combined total by 2030 and, toward this end, is expanding the development of carbon-free energy projects.

Regarding offshore wind power generation in Japan, which has been attracting attention, we were appointed as the operator for the project off the coast of Enoshima island, Saikai City, Nagasaki Prefecture, in December 2023 in a tender for selecting offshore wind power operators based on the Act on Promoting Utilization of Sea Areas in Development of Power Generation Facilities Using Maritime Renewable Energy Resources implemented by the Ministry of Economy, Trade and Industry and the Ministry of Land, Infrastructure, Transport and Tourism. We are currently proceeding with various surveys and design work in preparation for the start of commercial operation in August 2029, but we are also implementing various fishery promotion measures and regional development measures, aiming to be a business that is integrated with the local community.

Drawing on our long years of operational experience in solar, wind and biomass power generation, we are confident that we can contribute to the development of Japan's renewable energy power generation industry and the realization of a sustainable society.

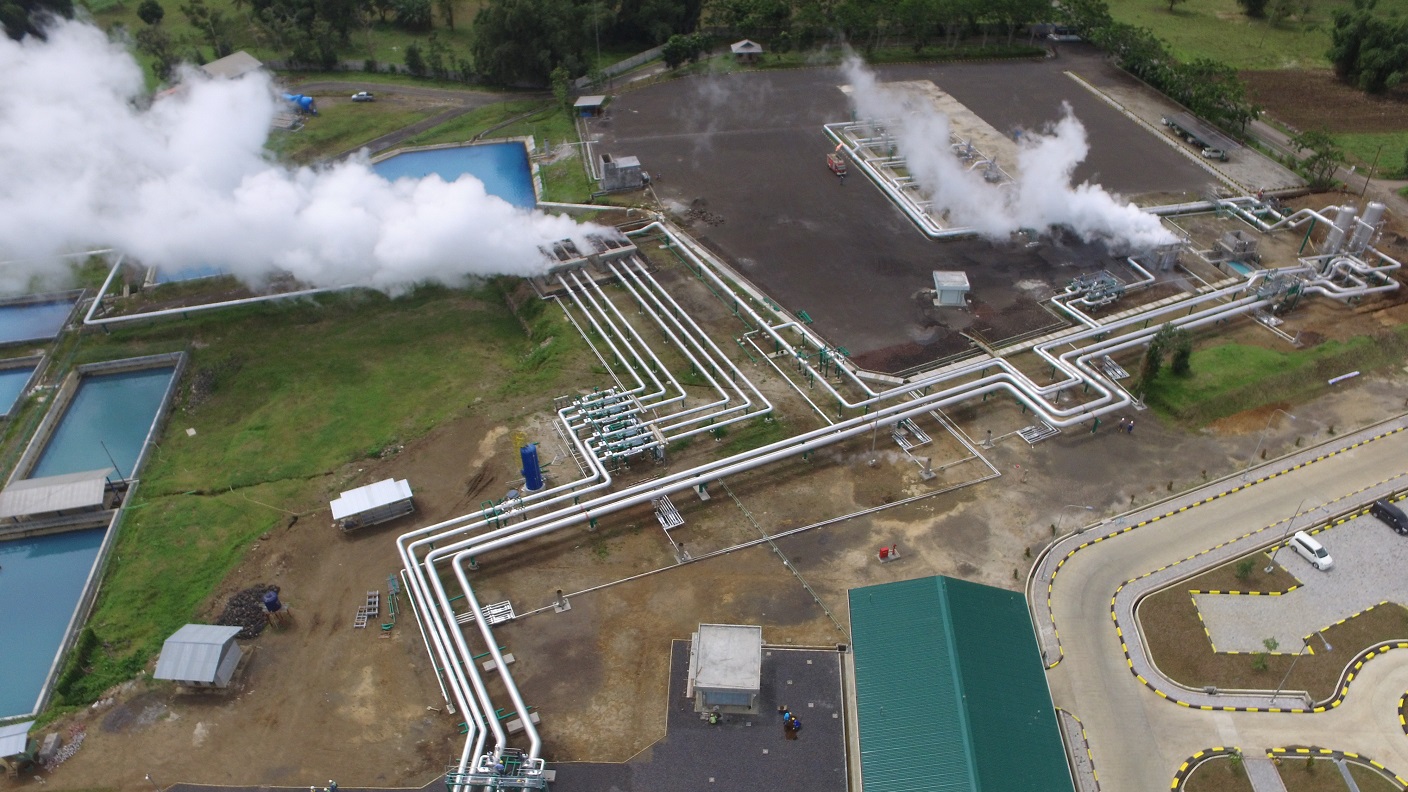

Geothermal power generation is a method used to generate electricity with a renewable energy source. The mechanism itself is simple: ground water is heated by deep underground magma near volcanoes, and the resulting steam turns the turbine of a generator that produces electricity. As it requires no fossil fuel consumption, geothermal power generation has a low environmental impact. Also, the cost of generating electricity is unaffected by fuel market fluctuations. Compared to other renewable energy sources such as solar and wind power, geothermal energy is undisturbed by climate conditions. Accordingly, this generation method can deliver electricity on a stable basis.

However, geothermal power generation entails some risks. It is unclear to know if enough hot water or steam (i.e. geothermal fluid) can be obtained for power generation until after a deep well has been drilled. In fact, some projects must be aborted as a result of drilling 2,000 to 3,000 meters in depth. Developing geothermal energy projects requires know-how of surface level surveys, ability to fund wells for drilling, ample time, and even a certain amount of luck.

Business models for power generation infrastructure are generally grouped into two main categories: EPC and IPP. EPC refers to construction contracts where the Engineering, Procurement, and Construction of a power plant are contracted. Under EPC arrangements, the contract is typically fulfilled when the completed facility is delivered to the local government or company. IPP stands for Independent Power Producer, where the operator becomes the owner of the generating facility and sells electricity on an ongoing basis.

With a view to the diversification of power sources in the future, Sumitomo Corporation has kept a keen eye on geothermal power generation since the early days when these projects were becoming larger in scale and more practical, and began delivering related equipment in the 1970s. Indonesia has the second highest number of geothermal resources in the world. We began our work in geothermal power generation there in 1995, and won our first EPC contract for a geothermal power plant in 1997. To date, we have been involved in a total of 12 projects (17 units totaling approximately 900 megawatts of power generation capacity). This represents 40 percent of the total geothermal capacity in the country and is the highest among Japanese integrated trading and business investment companies.

Our success with numerous geothermal EPC projects has been built on the productive partnerships we have forged. Our partners include Fuji Electric Co., Ltd. the world's leading manufacturer of steam turbines for geothermal power stations, and an Indonesian company PT. Rekayasa Industri, which take charge of civil construction, installation and local procurement. Among our recent geothermal EPC projects are the Lahendong power station in north Sulawesi and the Ulubelu power station in south Sumatra.

Our first geothermal IPP project in Indonesia was the Muara Laboh project, launched in west Sumatra in 2011.

Geothermal power stations are generally developed and built in untouched mountainous areas near volcanoes. Development of a geothermal project beings with construction works which consists of clearing and leveling the ground at the project site. Muara Laboh is located in a remote area, requiring four to five hours of overland travel from the nearest airport. In March 2012, the Project Company which Sumitomo Corporation along with its partners invests in entered into a long-term power purchase agreement over 30 years with the Indonesian state-owned electricity utility. After obtaining a Government Guarantee Letter from the Ministry of Finance of the Republic of Indonesia, the Project Company embarked on trial well drilling.

However, as a result of drilling exploration wells, the need to downscale power generation capacity became clear. We renegotiated with the Indonesian government and the Indonesian state-owned electricity utility regarding the terms and conditions of the project. It took nearly two years before all parties reached a unanimous agreement. The next step was to make financial arrangements for the actual power station construction. After five years of concluding the initial long-term power purchase agreement, we were able to achieve finance close and start the construction work in March 2017.

We were also contracted to provide EPC services for the construction of this plant. To achieve our goal of completing our first geothermal IPP project in Indonesia on time and contributing to the country's electricity supply, we not only leveraged our expertise as an operator that we have cultivated through other IPP projects, but also our extensive experience in geothermal EPC projects and the comprehensive strengths of our electric power infrastructure business as well. Finally, we were able to commence commercial operation in December 2019 and has since continued stable operation.

It was unprecedented for a Japanese company to be involved in the development of an Indonesian geothermal power project from the earliest stage, even prior to test drilling. Systemic difficulties made negotiations on project terms and conditions as well as financial arrangements a prolonged endeavor. Despite this obstacle, the successful completion of the power plant was achieved, helping us build a foothold for our next projects in Indonesia. Currently, based on the confirmation of surplus steam during the development of the Muara Laboh project, we are advancing a similarly sized expansion project adjacent to the existing power plant. After several years of negotiation with the Indonesian state-owned electricity company regarding the terms of the power purchase agreement, we were able to sign the amended power purchase agreement on December 2024, achieve finance close on April 2025 and start the construction work. The plant is scheduled to commence commercial operation in October 2027 and after the start of commercial operation, the electricity generated will be sold to the Indonesian state-owned electricity company for approximately 25 years until the end of 2025. Combined with the existing power plant, this project is expected to contribute to supplying electricity to the equivalent of approximately 900,000 households. In parallel, we are developing Rajabasa geothermal IPP project, another new initiative on Sumatra Island.

With the fourth largest population in the world at more than 270 million people, and an economy that continues to grow at around 5 percent per year, shifting to renewable energy and ensuring a stable supply of electricity have been national challenges for Indonesia. Geothermal power generation, which utilizes Indonesia's abundant geothermal resources, has been recognized as an effective means to simultaneously solve both of these issues, and the Indonesian government plans to increase its geothermal power generation capacity from the current 2,400 megawatts to 5,800 megawatts by 2030. The government is looking to Sumitomo Corporation, with its 20-plus years of experience in the construction of geothermal power plants and its experience in Muara Laboh geothermal IPP project, for support in this endeavor.

Geothermal power projects entail unique risks that other power sources do not. Building on our accumulated knowledge and expertise, we will contribute to the realization of a low-carbon society in Indonesia by managing those risks in cooperation with government agencies and financial institutions.

The European Union ("EU") aims to increase its use of renewable energy to at least 42.5% of the EU's total energy consumption by 2030. Under this circumstance, the development of offshore wind power generation projects is growing rapidly in Europe. This technology involves large turbines installed in the sea that harness the power of the wind to produce electricity. Wind farms are currently being constructed in earnest, mainly in the North Sea, which borders Norway, Denmark, Germany, the Netherlands, Belgium, France and the United Kingdom ("UK").

The greatest advantage of offshore wind power generation is the absence of physical obstacles to wind, such as mountains and buildings. This increases efficiency in energy conversion and facilitates output projection. The vast open spaces of the sea are also convenient for the transportation of turbine blades, a headache for onshore wind power projects situated on restrictive land sites. The North Sea is particularly suited to wind farms since shallow waters stretch out for over 40 kilometers off the coast.

Sumitomo Corporation entered the offshore wind power business in 2014. We participated in Belwind, Northwind and Nobelwind, Northwester2 wind farm projects, then in operation, under construction or in development in Belgium.

Constructing and operating these huge wind turbines requires stable funding, management skills to see the project through, and operational expertise. Having already accumulated considerable related experience through building and running conventional power plants and participating in onshore wind power projects in North America, China and South Africa, Sumitomo Corporation has been able to bring about successful outcomes in the Belgian projects.

Sumitomo's European bases for its offshore wind power business are Dusseldorf in Germany (European hub), London in the UK, and Paris in France. We have been exploring new business possibilities, working locally as an IPP firmly anchored in each locale and utilizing our global network as an integrated trading and business investment company to gather information.

In fact, it was due to our steady local efforts, in addition to our highly acclaimed role in the Belgian projects, that we were able to successively take part in two British offshore wind farm projects, Galloper in 2016 and Race Bank in 2017. Wind farms of Race Bank and Galloper, far larger in scale than their Belgian projects, were completed in March and September 2018, respectively. Sumitomo Corporation's experience and know-how accumulated through the Belgian projects is utilized in the operation of these British wind farms. Following them, we have started the new project Five Estuaries, an extension of Galloper.

In 2018, we took part in the Le Tréport and Noirmoutier offshore wind projects in France, following our participation in Belgium and the UK. Le Tréport project is located in the English Channel about 15 kilometers off the coast of France and Noirmoutier project is located in the Bay of Biscay about 12 kilometers off the coast of France. We achieved financial close* for both projects in April 2023 and are currently constructing the wind farms for operation. The two projects have a total power generation capacity of around 1 gigawatt, enough to meet the consumption needs of 1.6 million people.

As evidenced here, the European offshore wind power market is expanding year by year. Our goal is to expand our business in this field by increasing our participation in projects in European countries, including for floating offshore wind turbine farms, an area for which growth is expected going forward. Sumitomo Corporation is moving in this direction, pursuing greater stability in power generation and higher cost competitiveness, so as to ensure continuity of power supply in Europe.

Outside Europe, Asia, Oceania, and North America are attracting global attention for their lofty potential in offshore wind power generation.

In Asia, Japan, Vietnam and other countries are whose who draw much attention, not only because of its abundant wind resources over spacious oceans but also thanks to the government's commitment to renewable energy. Sumitomo Corporation applies the expertise acquired through the European projects to initiatives in Japan, especially for the offshore wind project in the sea areas off the coast of Enoshima Island, Saikai Chity, Nagasaki Prefecture of which we were appointed by the government of Japan (the Ministry of Economy, Trade and Industry and the Ministry of Land, Infrastructure , Transport and Tourism) to design, build and operate as the operator.

In April 2018, Sumitomo Corporation integrated its conventional power and renewable energy business segments and established a global system to enable it to work on power generation projects in a seamless fashion. The company's objective in this area is to establish a robust energy business that contributes to society and preserves the global environment for future generations.

In 2019, Sumitomo Corporation, Sumitomo Mitsui Banking Corporation and the Development Bank of Japan established the first fund through Spring Infrastructure Capital (SIC), a fund management company jointly established by the three companies. The fund—the first fund in Japan to invest in offshore wind power projects overseas—has acquired the UK-based offshore wind farms as seed assets (assets for investment by the fund). In 2022, SIC established a second fund to acquire solar power generation projects in Japan as seed assets.

Through SIC, we will provide institutional investors with opportunities to invest in renewable energy assets both in Japan and overseas, and contribute to the development of global infrastructure centered on renewable energy.

To protect our planet while guaranteeing the day-to-day comfort and convenience that electricity provides, Sumitomo Corporation continues to vigorously promote its renewable energy business.

Wood represents a recyclable resource because trees can be systematically planted, grown and harvested repeatedly. In addition, wood is one of our most familiar resources. Sumitomo Corporation started wood business by importing logs, lumber and veneer into Japan to support the high economic growth of the country. Since the 2000s, the Company has also expanded the business to include forest management, with a view to securing and utilizing forest resources in a more sustainable manner. We are also supplying wood products coming from the forests that we manage, targeting not only Japan's matured market, which does not have much room for remarkable growth, but also markets with high growth potential around the world.

Forests, which absorb and store CO2, can contribute to carbon neutrality across the globe through proper management and harvesting. Sumitomo Corporation also conducts sustainable forest management by practicing environment-friendly harvesting in the forests owned and managed by the Company. Looking ahead, we are committed to further expanding forest resources on a global scale while leveraging the expertise we have built in forest management.

In March 2013, Sumitomo Corporation acquired forest in New Zealand and subsequently began to manage it through Summit Forests New Zealand. The foreset extends over about 50,000 hectares on the North Island, where Radiata pine is grown and harvested to be exported to China and other Asian countries.

Forest management entails much labor, such as thinning out and pruning. There are also management risks to consider, including damage caused by fires and storms. Moreover, it might also be necessary to establish roads, ports and other infrastructure to transport harvested trees. Despite these challenges, Sumitomo Corporation is engaged in forest management in order to ensure a stable supply of wood on a long-term basis.

In Summit Forests New Zealand, trees are planted, grown and harvested in a cycle of 30 years to supply wood resources in an environment-friendly manner. For this forest, Sumitomo Corporation employs local inhabitants. They have long been engaged in and have vast knowledge of forestry. They are therefore efficiently sharing the work of planting, growing and harvesting trees in the plantation. On an annual basis, trees are hauled from the forest in the volume of about 600,000 m3 (equivalent to the volume of 900 25-meter pools). Nature is preserved in the forest, with wild horses running free.

Sumitomo Corporation is thus managing the forest in harmony with the local environment, instead of just trading wood from the forest, and this approach is highly evaluated by the local people. Also, we are applying advanced technologies to the industry, particularly to support harvesting operations. This involves employing drone and satellite photography systems to grasp the topographic features of plantation areas and to confirm the dimensions of harvesting areas.

We have entered power generation business using renewable energy, which is expected to grow as a medium- to long-term energy source, contributing to mitigating climate change.

As of March 31, 2025

| Fuel | Power plant | Country | Generation Capacity (MW) |

|---|---|---|---|

| Solar power | Osaka Hikarinomori Project | Japan | 10.0 |

| Solar Power Saijo | Japan | 29.0 | |

| Solar Power Kitakyushu | Japan | 16.0 | |

| Solar Power Tomakomai | Japan | 15.0 | |

| Solar Power Minamisoma/Kashima | Japan | 59.9 | |

| Solar Power Minamisoma/Haramachi | Japan | 32.3 | |

| EVM/EVM2 | Spain | 14.0 | |

| Thang Long Industrial Park (TLIP)/TLIPⅡ/TLIPⅢ | Vietnam | 25.1 | |

| Wind power | Oga Wind Power Plant | Japan | 28.8 |

| Summit Wind Power (Kashima) | Japan | 20.0 | |

| Abukuma Wind Power Plant | Japan | 147.2 | |

| Datang Sino-Japanese (Chifeng) New Energy | China | 50.0 | |

| Stanton Wind Energy | USA | 120.0 | |

| Cimarron Ⅱ Wind | USA | 131.1 | |

| Ironwood Wind | USA | 167.9 | |

| Dorper Wind | South Africa | 100.0 | |

| Mesquite Creek Wind | USA | 211.2 | |

| Amunet | Egypt | 500.0 | |

| Offshore wind power | Northwind | Belgium | 216.0 |

| Nobelwind | Belgium | 165.0 | |

| Northwester2 | Belgium | 219.0 | |

| Galloper | UK | 352.8 | |

| Woody biomass | Summit Handa Power | Japan | 75.0 |

| Summit Sakata Power | Japan | 50.0 | |

| Summit Myojo Power | Japan | 50.0 | |

| Sendai-ko Biomass Power | Japan | 112.0 | |

| Geothermal Power | Muara Laboh | Indonesia | 85.0 |

| Hydraulic power | CBK | Philippines | 792.0 |

In our real estate business, we have formulated and implemented basic policies related to environmental, social and governance (ESG) issues. As a part of this, from fiscal 2024, we have also begun allocating sustainable finance (※) to proceeds of office buildings and logistics facilities that have obtained real estate environmental certifications such as CASBEE and BELS.

In addition, Sumisho Realty Management Co., Ltd. (“SRM”), a group company of our company, has obtained real estate environmental certifications such as CASBEE, DBJ Green Building, LEED and BELS for its fund properties currently under management, including SOSiLA Logistics REIT, Inc. (“SLR”). Also, SLR has been awarded “5 Stars” in the 2024 GRESB Real Estate Assessment and the highest “A Level” for the GRESB Public Disclosure, which measures the quality of ESG disclosure.

As the first J-REIT to formulate a green finance framework since IPO, SLR has been promoting ESG-oriented asset management through green finance. SLR issued Green Bonds worth 1.6 billion yen in July 2022 and 3.0 billion yen in June 2023 with aims to strengthen the funding platform by expanding the ESG investor base, along with promoting ESG initiatives. Funds procured through Green Finance are used for the acquisition of existing or new assets (including scheduled acquisition) of Eligible Green Assets that satisfy any of the following eligible criteria, used for the renovation of Eligible Green Assets, or repayment and redemption of loans (including Green Loan) and Investment Corporation Bonds (including Green Bonds) required for these.

| Certifications | Property Name | Evaluation |

|---|---|---|

| CASBEE: 11 properties | SOSiLA Yokohama Kohoku | Real estate Rank A |

| SOSiLA Sagamihara | Real estate Rank A | |

| SOSiLA Kasukabe | Real estate Rank A | |

| SOSiLA Kawagoe | Real estate Rank A | |

| SOSiLA Nishiyodogawa I | Real estate Rank A | |

| SOSiLA NishiyodogawaⅡ | Real estate Rank A | |

| SOSiLA Ebina | Real estate Rank S | |

| LiCS Narita | Real estate Rank A | |

| SOSiLA Itabashi | Building (New Building) A Rank | |

| SOSiLA Amagasaki | Real estate Rank S | |

| SOSiLA Yashio | Real estate Rank S | |

| LEED: 1 properties | Atlanta Financial Center | SILVER |

| BELS:11 properties | SOSiLA Yokohama Kohoku | ☆☆☆☆☆ |

| SOSiLA Sagamihara | ☆☆☆☆☆ | |

| SOSiLA Kasukabe | ☆☆☆☆☆ | |

| SOSiLA Kawagoe | ☆☆☆☆☆ | |

| SOSiLA Nishiyodogawa I | ☆☆☆☆☆ | |

| SOSiLA Ebina | ☆☆☆☆☆ | |

| SOSiLA NishiyodogawaⅡ | ☆☆☆☆☆ | |

| LiCS Narita | ☆☆☆☆ | |

| SOSiLA Itabashi | ☆☆☆☆☆ | |

| SOSiLA Amagasaki | ☆☆☆☆☆ | |

| SOSiLA Yashio | ☆☆☆☆☆ |

To achieve sustainability management, companies need to develop a green transformation (GX) management cycle for the ongoing process of assessing their current GHG emissions, formulating GX strategies and measures, adopting GX solutions, and evaluating and revising the process. Sumitomo Corporation and ABeam Consulting have established a new joint-company called "GX Concierge Inc." to overcome climate change. Through this initiative, the company is developing a business that contributes to the promotion of GX in society by providing GX consulting services, GHG reduction solutions, and DX solutions.

Specifically, GX Concierge offers a variety of GX-related consulting services, including GHG emission calculations, support for information disclosure based on TCFD recommendations, short-term and long-term energy price forecasts, and the formulation of renewable energy procurement strategies. By providing various GX solutions that our group possesses to address the issues identified through GX Concierge's consultation, it supports the seamless promotion of GX for its customers. Furthermore, to meet the increasingly sophisticated needs of its customers, GX Concierge is expanding its services, including non-financial information disclosure based on SSBJ standards, TNFD recommendations, and the support for building circular economy initiatives.

Given our deep involvement in the supply chains of a wide range of industries, Sumitomo Corporation group will continue to aim for the realization of a sustainable society through GX Concierge, together with our suppliers and business partners.